Financial Literacy: Securing the Bag as a Young Medical Laboratory Scientist

How to Buy a House and a Car with your Internship Salary

AIM:

To equip young Medical Laboratory Science graduates in Nigeria, particularly those undergoing their one-year internship, with practical knowledge on earning and saving.

GIVEN:

Internship, Medical Laboratory Science, savings culture, budgeting, investment literacy, soft skills.

METHOD:

Expository essay

PRINCIPLE:

You’re a Medical Laboratory Scientist in your internship year. You're clocking into the lab early, staining slides, running tests, dodging passive-aggressive patient relatives, and literally trying to make it to the next week. As if that is not enough, the monetary reward for all your effort is barely enough to keep up with the constant expenses - and to make matters worse, it often shows up fashionably late. Can you relate?

Internship in Nigeria is a financial reality check. For many, it’s the first time earning a steady (albeit small) income and as such, a crash course in adulting. Between transportation, data, daily feeding, and the occasional craving to enjoy a bit of “soft life,” many interns find themselves living from alert to alert.

Take Chimezie as an instance. As is often the case, he waited thirteen long months after induction before securing an internship slot. When the placement finally came, he was thrilled. So, in the rush and excitement of new beginnings, he pledged to himself to save 40 per cent of his stipend. The first month goes by - nothing. He tells himself it’s fine; after all, the cost of relocation, (sparingly) furnishing a room, and settling in ate deep into the money. He shifts his savings goal to the next month. Then the next. And then the next, until it gets to the 12th month and he realises a whole year has gone by.

This brings to mind a haunting Igbo highlife line from an Nkwere Aborignes Women Club track:

“Okwu ụka si na ọmú nwa, e gbuo ru ya ewu ya. Okwu ụka mucha nwa, e rere ya ewu ya n’ahia. Okwu ụka nwa tụrụ chi ya uka, ụwa ọ dị gị ọlịa?”

A gabby woman who kept boasting that childbirth would earn her a goat slaughtered in celebration, only to end up selling her goat to cover delivery bills. For many interns, that’s exactly how it feels. A year that was supposed to be about building experience and laying a financial foundation turns into a cycle of unexpected bills, borrowing, and postponed plans. If one does not exercise adequate caution, it is easy to end up not just with zero savings, but neck-deep in debt. However, some interns and young people have managed to navigate this demanding year with a surprising level of financial control. How did they do it? What are they doing differently? What skills do you need to buy a car with your internship money - or, realistically, what must you start doing to stop it from vanishing mid-month?

PROCEDURE

My mother likes to say that money is a bird, that it has wings, and if you don’t trap it, it will fly. At first, I thought it was just one of those things Nigerian parents say to sound wise but as I started earning and spending on my own, I realised just how true it is. One moment, your account is heavy with that ‘whopping’ sum of ₦215,000, ₦175,000, or ₦130,000 (we see you!); the next, hunger is whopping you so hard that you're genuinely considering attending a different church just to pose as a first-timer - all for the free meal they offer. Suffice it to say that if you don't tell your money where to go, it will disappear without explanation. To prevent that unpleasant outcome from becoming your default reality, it helps to think of budgeting as a trap that keeps your money grounded.

1. BUDGETING

Inflows/Outflows

A good budget starts with understanding your cash flow. You need to know exactly how much is coming in and where it is going. For most interns, this includes your monthly stipend, gifts and sometimes the occasional “urgent ₦2k” from family or side gigs. Track every expense for at least a month from the ọkada (bike) fare and lunch snacks to your data subscriptions and if-I-perish-i-perish impulse spendings. Most of us underestimate how much we spend on little things until we see it written down. Earlier this year, I decided to note down every naira that left my account for two months. I saw where my money was leaking and that gave me clarity, yes - but fair warning: this tip is sobering.

Choosing a Budgeting Framework

Once you are aware of your income and expenses, the next step is choosing a budgeting method that suits your lifestyle. A modified 50-30-20 rule works well: you allocate 50 per cent of your income to needs like feeding, cooking gas, transport and data, 30 per cent to wants like Netflix, hangout with friends, and 20 per cent to savings or debt repayment. Of courses, for interns living in expensive cities like Port Harcourt, Lagos, or Abuja without an additional stream of income, this might shift to 60-25-15. Another useful method is zero-based budgeting, which means you allocate every naira to a purpose, so your income minus expenses equals zero. This ensures intentional spending. Some also adopt the envelope method, physically dividing their cash or using digital wallets/apps to keep spending in check.

Set Specific Goals and Automate

Setting realistic financial goals is essential. It is enough to just go about chanting, “I want to save.” A specific declaration would be: “I want to save ₦10,000 every month for an emergency fund” or “I want to commit ₦20,000 every monthly for post-internship life”. Once that is clear, automate it. Tools like PiggyVest, Cowrywise, and even some bank apps allow you to set standing orders that move money into your savings before you are tempted to spend it.

Do not forget to make an allowance for miscellaneous spending or budget busters like charger replacement, family contributions or even hospital supplies (for interns that work in poorly equipped facilities). So, also include “sinking funds”; small reserves built over time for predictable but irregular expenses.

Eat Your Cake, Have it Back

Finally, remember that budgets are not carved in stones. What worked in January might not hold up in June when fuel prices double or when data tariffs are higher. Review your spending monthly. If, for instance, you find that eating out is draining your budget, it might be time to reconsider your habits. Cooking at home can help - but with today’s prices and increasing food inflation, even that can feel just as expensive unless you are buying your ingredients in bulk.

Two interns I spoke to shared that bulk buying significantly reduced their weekly food expenses. Purchasing staples like rice, garri, or beans from local markets, especially in larger quantities, helps cut down on unit costs and reduces the need for constant top-ups. You save more when you plan ahead. To stretch your savings further, try meal-planning for the week. It helps you avoid last-minute takeaways and keeps you intentional about what you eat - and spend. You can take it a notch further by identifying if there are any ‘bush markets’ in your area where farmers sell directly to consumers at cheaper rates. These markets often offer fresher produce at a fraction of the cost you would find in regular retail spaces. Talk about eating your cake and having it back!

2. SAVINGS

Start However

Saving as an intern in 2025-Nigeria may feel like wishful thinking but the truth is: if you do not make saving a habit now, it gets even harder when you start earning more. That is because saving is less about how much you earn and more about how disciplined you are with what you have. So, annihilate the mindset that you need a “big break” before you can start saving.

Pay Yourself

A good place to start is the “pay yourself first” principle. This means setting aside a portion of your income, no matter how small, before you spend on anything else (this, by extension, implies that saving must be done immediately because again, money is a bird). Saving as little as ₦1,000 weekly adds up to ₦52,000 a year; enough to register a business name, take an online course, or attend a paid conference, right? The key at this stage is consistency, not volume.

A smart step is to separate your savings from your daily spending. DO NOT save money in the same account you use to buy Oceanic bread at night. Digital saving platforms like PiggyVest, Cowrywise, or even a second traditional bank account with no ATM card help create separation between your spending money and your savings. Some of these apps allow you to automate your savings and even lock funds away to reduce temptation. Side note: try not to always be the person that breaks their piggy banks to help people who just would not touch theirs. What if they genuinely need it? Well, refer back to the line about “sinking funds”.

"Regardless of the magnanimity of your heart, resist the urge to break your savings to help everyone you meet. And in helping people, never lend money you can not afford to forfeit.”

Personally, I make exceptions only for close friends who have consistently proven themselves financially trustworthy.

Label Your Savings

Give your savings a name. Labels help you stay focused. “Emergency fund” adds urgency. “Graduate School Application 2026” makes the goal tangible. “Owambe dress fund”? Still valid. It all depends on your priorities at the time. When your savings have a purpose, you are more likely to stick to the plan.

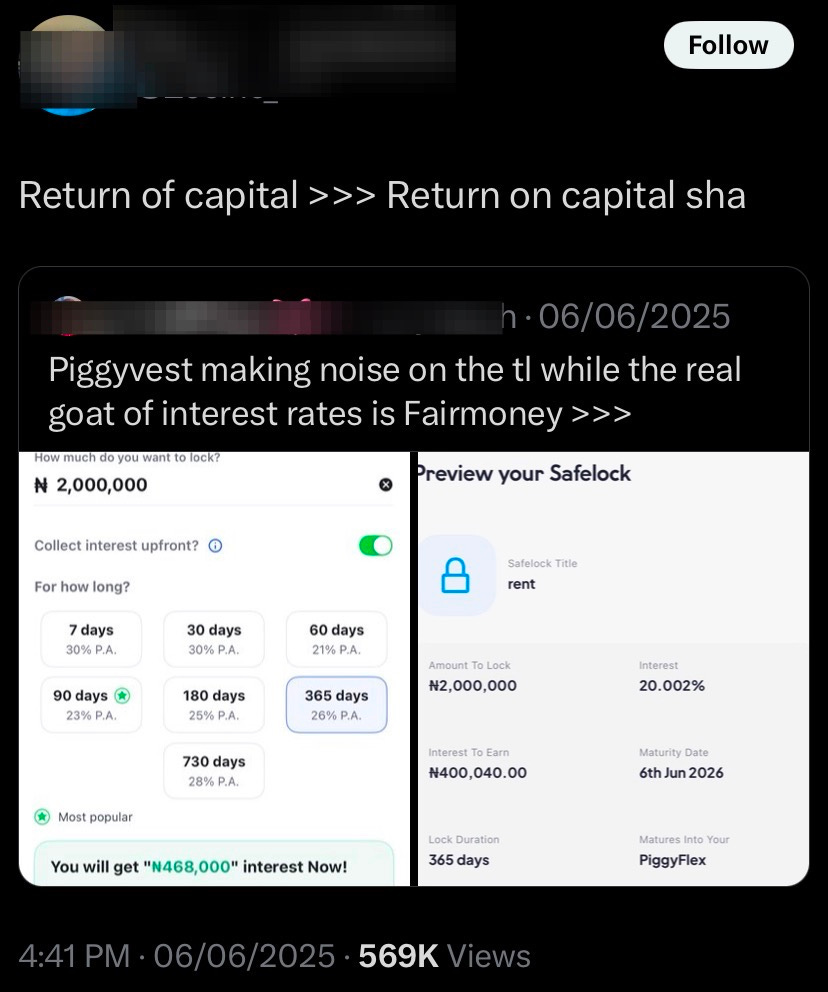

You can also explore rotating thrift groups, known locally as ajo, akáwò or esusu. These community-based systems encourage discipline by holding you accountable - but only join groups with people you trust as much as your study partner back in school. If possible, there should be a signed agreement between all parties involved. A failed ajo can hurt more than an overstretched debit card. Or like one twitter (now X) user humorously remarked: “return of capital is better than return on capital”.

3. INVEST, BUT….

After building the habit of saving, the next step is learning how to grow your money. In an economy like Nigeria’s, where inflation reduces the value of cash over time, investing is one of the few ways to protect and increase your financial standing. However, it must be done with care.

A common mistake is jumping into ventures you do not fully understand because someone you know is doing it. From real estate syndicates to agrotech platforms and crypto schemes, it is very easy to get swept up in hype. The golden rule is: only invest in what you understand. If you cannot explain how the money grows or where the risks lie, you are better off staying away. If you cannot explain the business model to a friend in simple terms, do not put your money there. Before you invest money, invest time in learning. It is that simple really.

Platforms like Cowrywise, PiggyVest, Bamboo and Rise offer entry points as low as ₦1,000 into treasury bills, mutual funds, and even dollar savings. They are regulated and relatively safe for beginners, but always read the fine print. Don’t just trust vibes and screenshots. And that deep fakes are easier to circulate, you may want to exercise the caution of the famous Thomas who doubted even the one of the greatest men to have walked our earth.

When Not Sure, Choose Yourself

Investment extends beyond financial products. So, consider “investing” in your skills, tools or knowledge that can boost your earning power. A ₦10,000 course, design software subscription, health-based certification, or baking equipment could give you better returns in the long run than trendy ventures with unclear models. Therefore, begin with caution and always do your own research.

Building wealth takes time - and internship is exactly the right time to build the habit. And remember, if the offer sounds too good to be true or comes with urgency, it’s probably a scam.

4. STACK SKILLS THAT INCREASE YOUR MARKET VALUE

Medical Laboratory Science provides a solid foundation, but adding relevant soft and digital skills can multiply your earning potential. Explore short courses (some are free or subsidised) in:

Coding or transcription (great remote job options)

Health data analytics (Excel, SPSS, Power BI)

Science communication and grant writing

Project management (CAPM, Agile/Scrum basics)

Basic design or digital storytelling (Canva, storytelling for health)

Bioinformatics

Molecular biology and genetics

Platforms like Coursera, edX, FutureLearn, openWHO, and LinkedIn Learning have accessible and affordable options. Even if you dedicate just 3 hours a week, you’ll be surprised at how much you can learn (and eventually earn). There’s also opportunity in technical niches - like servicing lab equipment or exploring the health tech space. Labs and health startups alike value MLS professionals who bring something extra to the table. The MLS journey is long but the earlier you start stacking relevant skills, the faster you position yourself for financial growth - both within and beyond the profession.

5. ‘PACKAGE’ YOUR KNOWLEDGE

Are you already feeling overwhelmed by the thought of having to learn any of the aforementioned skills? I know that feeling too well, so here's a piece of goodnews: sometimes, the most valuable skills are the ones you’ve had all along; you just have not figured out how to sell them yet. Maybe you write well, design flyers for your fellowship, or your classmates always ask you for help with understanding histology slides. That’s a starting point.

You do not even need to be the best at a skill to earn from it - just better than the person who needs your help. Can you simplify difficult concepts? Start creating study guides or offer tutorials. Good at Canva? Offer to design flyers or social media graphics for small businesses. Are you a natural organiser? Look into virtual assistant gigs or event coordination roles. If you are great at speaking, explore voiceovers or MC-ing events.

These may not sound “serious,” but they’re real sources of income for many young people today. Personally, I know two brands that make calls for an earning - you read right! Want to call someone who you pissed off? Great. Birthday shout-outs? Active! Want to let your loved ones know you think they are the next best thing after Afang or Oha soup? They've got it! And people are paying, yes.

For academic services: proofreading project work, editing essays, designing PowerPoint slides, formatting CVs, or writing statements of purpose (SOPs) are tasks fellow interns - and others- will happily outsource if you offer clarity and quality.

Got a flair for content? Science communication is a goldmine. You can create short videos breaking down lab tests, busting health myths, or explaining disease trends. TikTok, YouTube, and Instagram have growing communities interested in smart, simple science content - but then again, you need to really be patient to grow in this field.

Freelance writing is a trusted outlet (if I do say so myself). You can write for or contribute to science blogs, health NGOs, or websites. Your lab stories, research insights, and practical knowledge are content gold.

Social media is your friend here. Platforms like Twitter, LinkedIn, Instagram, and WhatsApp can help you promote your service to the right audience. Remember, packaging is everything. "Waste Management Officer" vs "Dustbin Collector" - potato potatoes. "Personal Shopping Consultant" vs "Errand Girl”. Same difference! People don’t just pay for what you know - they pay for how you present it. Stop selling yourself short.

6. SHOW UP AND SHOW OFF

Realistically, many opportunities are not advertised - they’re recommended. Start seeing networking as intentional relationship building, not just LinkedIn follows or conference selfies. Make sure people walk away with a clear sense of who you are, what you do, or what you’re passionate about - or at the very least, a curiosity to learn more.

Engage with your senior scientists, fellow interns, your hospital’s consultants. Join MLS-related WhatsApp/Telegram groups and participate. Attend seminars, both online and offline. And when in such spaces, speak up, ask questions, follow up with speakers. Let your curiosity be your currency.

Post on social media, particularly LinkedIn. Share your internship wins. Document your learning journey. Do not feel awkward about reaching out to alumni who are doing work you admire. Your next job, scholarship, or partnership might come from a strategic “hello” you typed today or from someone who saw your name pop up consistently doing meaningful work.

COMMENTS

The same way small bacteria can cause massive infections, you should understand that small financial actions can cause massive breakthroughs. So, basic financial literacy is key. For this purpose, MedLabConvo will be hosting a finance literacy series on 21st June, 2025.

Register here.

Lastly, you’re not “just an intern.” You’re a scientist-in-the-making-and your bag is waiting.